turk_stock_photographer

Most STORE Capital investors (NYSE: STOR) were likely surprised to see a more than 20% gain in the stock on the morning of September 15, then to learn that it was acquired by real estate giants GIC and Blue Owl’s Oak Street in a $14 billion all-cash transaction, or $32.25 per share.

Shareholders may have mixed feelings about the takeover. On the one hand, they may enjoy the instant gratification of a 20% gain in one day, allowing them to deploy the gains into other investments. On the other hand, they may have bought STOR with the intention of securing a long-term recurring revenue stream, and the deal takes them away.

Additionally, investors who have acquired shares of STOR within the last 12 months must pay tax on their short-term capital gains (taxed at the ordinary income rate) and for shares held over 12 months, must pay long-term capital gains of at least 15% (assuming they earn at least $40,000 per year if single). Investors who bought above $32.25 will just have to take a loss assuming the deal goes through, more on that later.

But just like in life, we live with the cards that are dealt to us in the world of investing, and it’s important to weigh the options. This article sheds light on what shareholders can do now with a deal on the table.

STOR has a takeover deal – now what?

For those unfamiliar with the company, STORE Capital is a company founded by former CEO Christopher Volk. It’s the third REIT he’s helped guide to an IPO (two of which he co-founded). Its goal is to own single-tenant operational real estate that is profit centers, making it more valuable in the eyes of its tenants.

Currently, it has a diversified portfolio of 3,000 properties in 49 US states, most of which are related to the service sector (think e-commerce resistance). Additionally, STOR obtains unit-level financial reports from the vast majority of its properties, giving it line of sight and the ability to resolve tenant issues before they become problems.

Net lease REITs have seen significant weakness in their stock prices over the past month. For example, Realty Income (O) is now trading at $64.33 with a forward P/FFO of 16.0, well below its short-term high of $75 from as recently as August. which equates to a forward P/FFO of 18.7. This drop in market favor is likely due to investor concerns about stubbornly high inflation in perceived slower-growing net rental REITs.

The fact is, however, that STOR has been one of the fastest growing net rental REITs, generating a CAGR of 5.9% AFFO/share since its IPO 8 years ago. Additionally, management has guided an impressive 9.8% to 10.7% growth in AFFO per share this year, outpacing the rate of inflation the US economy has seen so far this year.

One of the main reasons for this impressive growth is a greater reliance on internal funding sources, as STOR has a dividend payout ratio of just 66% (based on a Q2 AFFO per share of $0.58). As such, STOR does not need to have a high stock price to generate growth through equity issues, nor is it entirely at the mercy of debt markets when rates interest increases.

Sure, it would be nice to have a high share price and low cost of debt as sources of funding for growth, but the fact is that STOR can still grow without those characteristics. Additionally, the reduced reliance on external funding sources allows STOR to better position itself during bear markets as it can outbid the higher leveraged private equity players in the space with attractive capitalization rates.

Given these attributes, I believe the deal on the table for STOR at $32.25 with a forward P/FFO of 14.66 fundamentally undervalues the company. It seems the market thinks so too, as the stock price has been offered as high as $31.95 (it was $32.20 yesterday). This only represents a stock price appreciation of $0.30 plus a dividend payment of $0.385 based on the current transaction price.

As such, it seems the market thinks (but without guarantee of course) that there could be another bidder for STOR within the 30 day time frame. I believe STOR is worth $38.50 per share in a all in cash redemption scenario. This represents an advanced P/FFO of 17.5x and would bring all shareholders who have bought in the last 12 months out of the water.

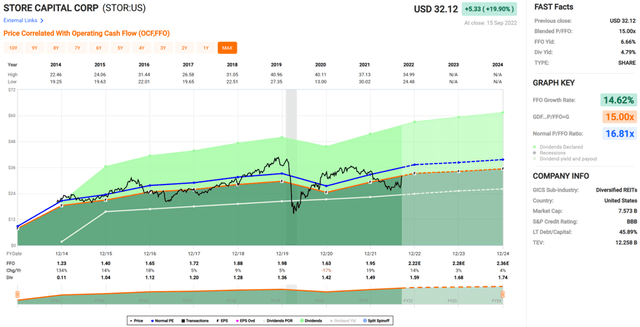

It may be wishful thinking and it may never happen, but I think it’s reasonable, given that it represents a moderate premium to fair value and would offset taxes on capital gains. capital that investors must pay in an all-cash transaction. As shown below, STOR has traded at a normal P/FFO of 16.8 since inception.

STOR valuation (FAST Charts)

So what should an investor do now? Those who think the overall market will remain weak for the next 30 days can take a wait-and-see approach to see if a better offer materializes. Or, they can possibly wait out the term of the deal, with the possibility that shareholders will reject it.

For those who have had enough and just want to cash in now, I consider Realty Income (O) and National Retail Properties (NNN) to be solid options. Realty Income comes with an A- rated balance sheet and a healthy and growing yield of 4.6%, while NNN comes with a 5% yield with a BBB+ rated balance sheet. For those with more risk appetite, Spirit Realty Capital (SRC) has a dividend yield of 6.3% and trades at a P/FFO of just 11.5.

Key takeaway for investors

Market prices on STOR seem to indicate the belief that a better offer might come along. Additionally, the tax considerations of an all-cash transaction make it unattractive, especially to retail investors. Those who think a better deal could be struck may want to hold on to their shares. It is also possible that shareholders will not approve of the deal. For those who think the deal is fair, or who just want to cash in and want to stick with net rental space, O, NNN and SRC present solid alternatives at their current prices.